A7A5 and the new sanctions plumbing

Published

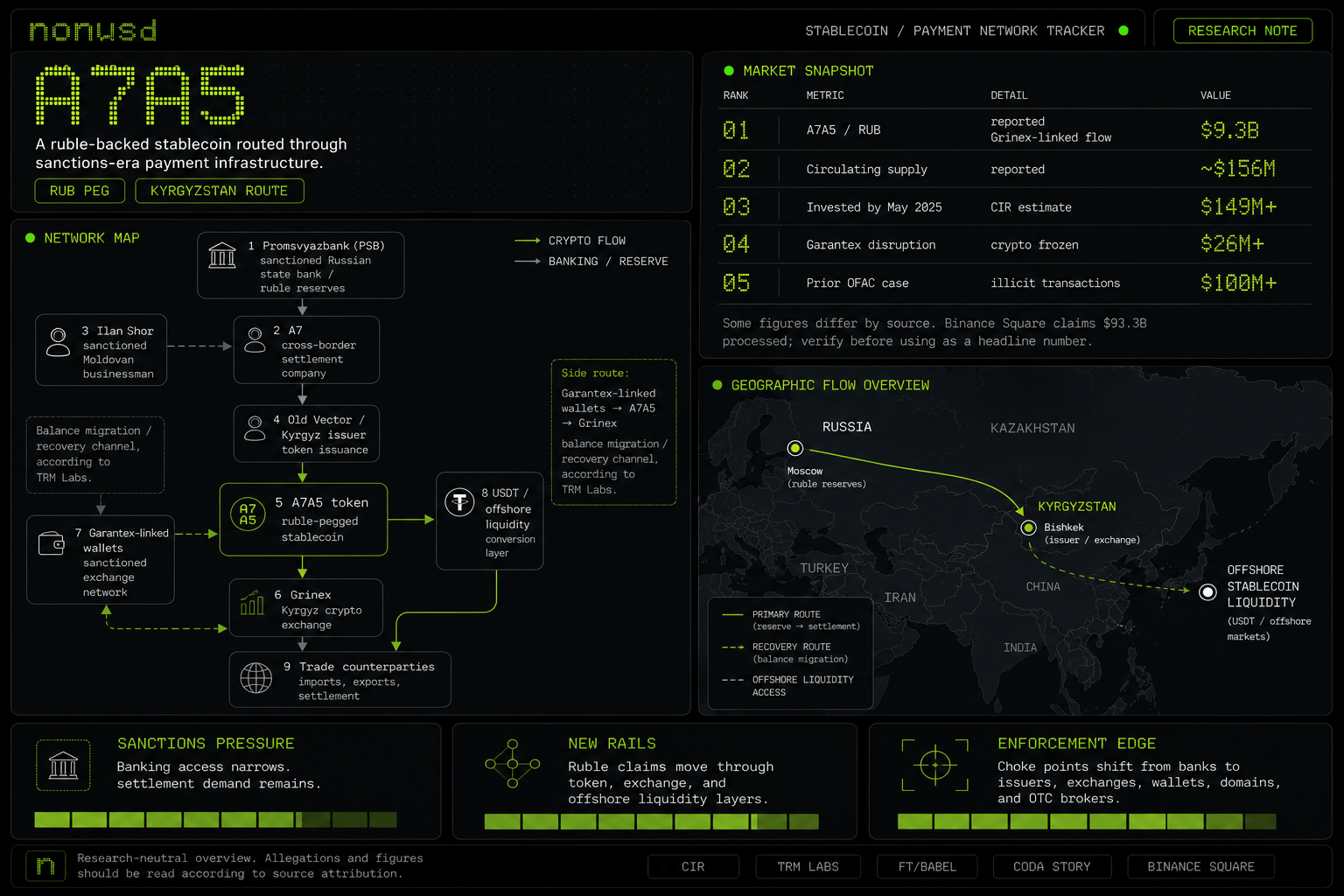

Where the A7A5 story touches the map

Exchange and legal corridor

Kyrgyzstan is where the token issuer / exchange corridor becomes operational surface area.

Old Vector and Grinex are central to the Kyrgyzstan routing story in the article.

A7A5 price and trading activity over the last 30 days

Uses the same CoinGecko market data already powering the coin detail pages. Price is shown as the line; daily trading activity is shown as the bar layer.

A tighter chart to make short-range peg drift legible without forcing the reader to inspect the separate coin page.

Evidence from the Dune dashboard snapshot behind the article

On-chain activity source: Dune Analytics dashboard snapshot attributed to @dkhol in the provided image.

Use it as directional evidence for activity concentration and timing, not as final attribution of beneficial ownership.

Wallet tables indicate concentration among a small set of high-volume addresses, which supports the article’s corridor thesis.

Top receiving wallets

Top sending wallets

Subtitle: A ruble-backed stablecoin, a Kyrgyz exchange corridor, and the strange afterlife of Garantex show how financial pressure creates new monetary infrastructure.

Byline: NonUSD Research Desk

There is a familiar rhythm to sanctions.

A state or enforcement agency blocks a bank, exchange, shipper, oligarch, or payment network. The target loses access to a piece of the formal dollar system. For a while, the pressure works. Money gets stuck. Counterparties hesitate. Banks over-comply. Then, somewhere on the edge of the map, new plumbing appears.

A7A5 looks like one of those pipes.

The token is marketed as a ruble-backed stablecoin. Its public pitch is simple enough: one digital token, tied to the Russian ruble, backed by ruble deposits, usable for cross-border settlement where conventional banking channels have become slower or unavailable. The more interesting story is not the peg. It is the network around it.

According to reporting and blockchain intelligence work from the Financial Times, Babel, the Centre for Information Resilience, Coda Story, TRM Labs, and others, A7A5 sits at the intersection of several post-2022 trends: Russian sanctions pressure, the migration of high-risk crypto activity away from exposed venues, Kyrgyzstan’s emergence as a useful financial waypoint, and the search for stablecoin rails that do not depend directly on U.S. banks.

That does not mean every use of A7A5 is illicit. Nor does it mean that stablecoins are inherently sanctions-evasion tools. The point is narrower and more interesting: when an economy is pushed out of the dominant settlement layer, it starts looking for another one. Sometimes that alternative looks like barter. Sometimes it looks like gold. Sometimes it looks like a bank in a friendlier jurisdiction. And sometimes it looks like a ruble stablecoin trading through a new exchange with familiar fingerprints.

Solid arrows show controlling ownership or ruble reserve flow. Dashed arrow shows reported balance migration from Garantex-linked wallets into A7A5 (TRM Labs).

The actors around the token

The corporate center of the story is A7, a Russian company reportedly created in October 2024 to facilitate cross-border financial transfers for Russian clients under Western sanctions. CIR describes A7 as majority owned by Ilan Shor, the Moldovan political figure and businessman who has been sanctioned and convicted for fraud in Moldova. A7 is also described as minority owned by Promsvyazbank, or PSB, a sanctioned Russian state-owned bank associated with Russia’s defense sector.

In January 2025, A7 and PSB announced A7A5 in Kyrgyzstan. The token was promoted as the first stablecoin pegged to the Russian ruble and backed by fiat ruble deposits in PSB accounts.

That backing structure matters. Most stablecoins that trade globally are synthetic dollars: USDT, USDC, FDUSD, and others. Their utility comes from giving users dollar-like settlement without requiring a traditional bank transfer every time value moves. A7A5 takes the same basic stablecoin design and flips the currency unit. Instead of dollar stability, it offers ruble stability. Instead of sitting naturally inside the U.S.-linked dollar ecosystem, it appears designed for a world where Russian counterparties need a bridge out.

CIR estimated that at least $149 million had been invested in A7A5 as of May 2025. Babel, citing the Financial Times, reported that wallets linked to the Grinex exchange had moved about $9.3 billion worth of A7A5 in four months, while only around $156 million worth of tokens were reportedly in circulation. That gap is worth pausing on. A small float can support very large transaction volume if the same units turn over repeatedly.

A Binance Square post claims much larger numbers, including $93.3 billion processed through the channel and $2.2 billion through instant exchange services. Because this figure differs materially from the FT/Babel number, it should be treated carefully unless corroborated by primary chain analysis or a named intelligence report.

Verified or single-named-source figures only. The $93.3B Binance Square claim sits roughly 10× above the FT/Babel number and is excluded here pending corroboration.

Roughly sixty times turnover in four months on a small float — a signature of repeated settlement, market-making, or balance migration rather than user holding.

The Garantex afterlife

The other name running through this story is Garantex.

Garantex was a crypto exchange with deep ties to Russia’s high-risk crypto economy. OFAC sanctioned it in April 2022, saying it had facilitated more than $100 million in illicit transactions, including ransomware payments and darknet market flows. TRM Labs says Garantex remained responsible for a large share of crypto volume moving to and from sanctioned entities and jurisdictions after its designation.

Then came March 2025. A multinational action seized Garantex’s main domain and froze more than $26 million in cryptocurrency. This looked like a serious disruption. But crypto networks do not die the way banks die. They fork, rebrand, rotate domains, move users, and find new interfaces.

TRM Labs reports that Grinex, a successor-like platform incorporated in Kyrgyzstan in December 2024, appeared almost immediately after the Garantex action. Telegram channels linked to Garantex reportedly promoted Grinex as a “new platform with familiar functionality.” TRM says Grinex reproduced elements of Garantex’s interface and operational model and worked to onboard former Garantex customers.

A7A5 enters here as a settlement and recovery instrument. TRM says former Garantex users were credited A7A5 in amounts equivalent to frozen balances, which they could then trade or redeem on Grinex. TRM also reports that Garantex wallets began moving funds into A7A5 as early as January 2025, before the March enforcement action.

If accurate, that timeline suggests preparation rather than improvisation. The token was not merely a financial product that happened to become useful after Garantex was hit. It may have been part of a contingency architecture.

Why Kyrgyzstan matters

Kyrgyzstan is not incidental to this story.

Coda Story frames Bishkek as a potential backdoor jurisdiction, not because Kyrgyzstan is unique, but because it fits an old pattern. When large pools of money face restrictions in one part of the system, they look for smaller jurisdictions willing to provide legal surface area, corporate registration, banking relationships, and political ambiguity.

That role has been played, in different ways, by Switzerland, Hong Kong, Dubai, the Cayman Islands, Delaware, and many others. The names change. The function does not.

Kyrgyzstan has already appeared in reporting about Russian sanctions circumvention through trade transshipment. Coda notes the movement of goods through Kyrgyz companies to help Russian buyers access restricted products, including luxury cars. Crypto adds a faster layer. If a jurisdiction can host exchanges, token issuers, payment intermediaries, and corporate shells, it can become a settlement node without needing to be a major financial center.

This is where A7A5 becomes more than a coin. A ruble token in isolation is not very useful. A ruble token with exchange venues, redemption paths, friendly banks, corporate wrappers, and connections to larger stablecoin liquidity pools becomes more interesting.

That is also where the sanctions question gets complicated. A token like A7A5 does not need to break the dollar system. It only needs to route around the specific choke points that sanctions rely on.

Top path is the conventional correspondent-banking route. Bottom path is the substitute settlement layer that A7A5 and Grinex assemble.

How a ruble stablecoin can support sanctions evasion

The basic sanctions-evasion use case is not mysterious. A sanctioned or high-risk actor needs to move value across borders. Traditional banks either cannot touch the transaction or do not want the risk. A crypto rail provides a substitute settlement layer.

A7A5 could support that in several broad ways:

First, it can transform trapped ruble liquidity into transferable digital claims. Rubles inside a sanctioned bank are hard to move internationally. A tokenized claim on ruble deposits can move across blockchain addresses and exchange accounts much more easily.

Second, it can provide a bridge between Russian counterparties and non-Russian intermediaries. A supplier, broker, or trade agent that does not want direct exposure to a sanctioned Russian bank may still interact through an exchange or offshore entity that handles the token leg.

Third, it can create turnover far above its circulating supply. The reported contrast between roughly $156 million in circulation and billions in volume suggests repeated use for settlement, market-making, or balance migration.

Fourth, it can connect to larger crypto liquidity. A ruble stablecoin by itself is parochial. But if it can be exchanged into USDT or other liquid tokens, it becomes part of the broader offshore crypto economy.

Fifth, it can preserve user relationships after enforcement actions. The Garantex-to-Grinex transition, as described by TRM, suggests that A7A5 was useful not only for external payments but also for restoring balances, migrating clients, and keeping a sanctioned exchange network alive under new branding.

That is the part regulators tend to underestimate. Crypto exchanges are not just websites. They are customer graphs, Telegram channels, wallet clusters, OTC relationships, habits, trust networks, and informal credit systems. Take down the front door and the crowd may move to a side entrance.

The neutral read

There are two lazy ways to write about A7A5.

The first is to treat it as proof that crypto is only useful for criminals. That misses the point. Stablecoins are useful because they settle quickly, cross borders easily, and reduce dependency on slow correspondent banking. Those properties are valuable to migrant workers, traders, fintechs, inflation hedgers, and ordinary users in weak banking systems. They are also valuable to sanctioned entities. The tool is not the motive.

The second lazy reading is to pretend this is just neutral technology and that sanctions policy has nothing to do with it. That also misses the point. A7A5 appears to have been built in a very specific geopolitical context. Its ownership, banking links, exchange relationships, and timing all point toward a payments architecture designed for a Russia under financial pressure.

A more honest reading sits in the middle: A7A5 is a case study in how monetary systems adapt under constraint. Sanctions create scarcity in settlement access. Markets respond by manufacturing new settlement access. Some of that activity is legal trade searching for a path through over-compliance. Some of it is plainly illicit. Much of it lives in the gray zone where enforcement agencies, blockchain analytics firms, banks, and exchanges spend their days arguing over intent.

That gray zone is where the story lives.

What regulators can and cannot do

The obvious response is designation. OFAC and allied agencies can sanction issuers, exchanges, wallet addresses, directors, banks, and affiliated companies. They can seize domains, freeze assets held through cooperative platforms, and pressure centralized exchanges to block flows.

That works when the network touches compliant infrastructure. It works less well when activity moves through jurisdictions that do not cooperate, through self-custodied wallets, or through venues with little U.S. exposure.

This is the cat-and-mouse structure of modern financial enforcement. The U.S. and EU have enormous power over banks, dollar settlement, regulated exchanges, and companies that care about Western markets. They have less power over entities that already assume they are outside that system.

A7A5 tests that boundary. If the token’s main backing sits in a sanctioned Russian bank, its issuer is in Kyrgyzstan, its users are already high-risk, and its trading venues have limited Western exposure, the normal levers may be weaker. Enforcement can still raise costs, identify wallets, stigmatize counterparties, and make liquidity harder to access. But it may not stop the network outright.

The better question is whether the system can keep converting A7A5 into useful external value. A ruble token that only circulates among sanctioned actors is a closed loop. A ruble token that can reliably touch USDT, fiat brokers, trade intermediaries, or commodity flows is a bridge.

The bridge is the thing to watch.

The larger stablecoin lesson

A7A5 is not likely to become a global reserve instrument. It does not need to. Its importance is narrower: it shows that stablecoin architecture is being localized, weaponized, and adapted for non-dollar monetary blocs.

For years, the main stablecoin story was dollarization. USDT and USDC exported the dollar to crypto markets, offshore exchanges, emerging economies, and people living with weak local currencies. A7A5 points in a different direction. It suggests that sanctioned or semi-isolated economies may try to build their own stablecoin rails, not to replace the dollar globally, but to avoid needing it at specific moments.

This is a more fragmented future. Dollar stablecoins continue to dominate liquidity, but regional and politically aligned tokens appear where dollar access becomes unreliable. Some will be state-backed. Some will be bank-backed. Some will be exchange-issued. Some will be little more than compliance arbitrage with a ticker.

The old offshore system was made of shell companies, nominee directors, private banks, trade invoices, and patient lawyers. The new one adds tokens, wallet clusters, instant swaps, and exchange migrations. The purpose is familiar. The interface is new.

A7A5 may fade, get sanctioned into illiquidity, or be replaced by a cleaner successor. But the pattern will stay. Financial pressure does not eliminate demand for settlement. It redirects it.

And in that redirection, new monetary infrastructure gets built.

Sometimes in the open. Sometimes through Bishkek.

Source notes

- Binance Square — “Tracing the Path of Stablecoin A7A5 Rescuing Billions of Dollars Under Sanction.”

- Babel / Financial Times — “Fugitive Moldovan oligarch Ilan Shor founded a cryptocurrency to help Russia circumvent sanctions.”

- Coda Story — “Crypto’s backdoor through Bishkek.”

- Centre for Information Resilience — “A7A5: Circumventing sanctions with stablecoin cryptocurrency.”

- TRM Labs — “Garantex, Grinex, and the A7A5 Token: A Deep Dive into Sanctions Evasion Networks.”

Editorial caveat: Some reported numbers differ across sources. The $9.3 billion figure appears in Babel’s summary of FT reporting. The Binance Square post claims $93.3 billion, which should be verified before publication or framed as an unverified claim from that post.